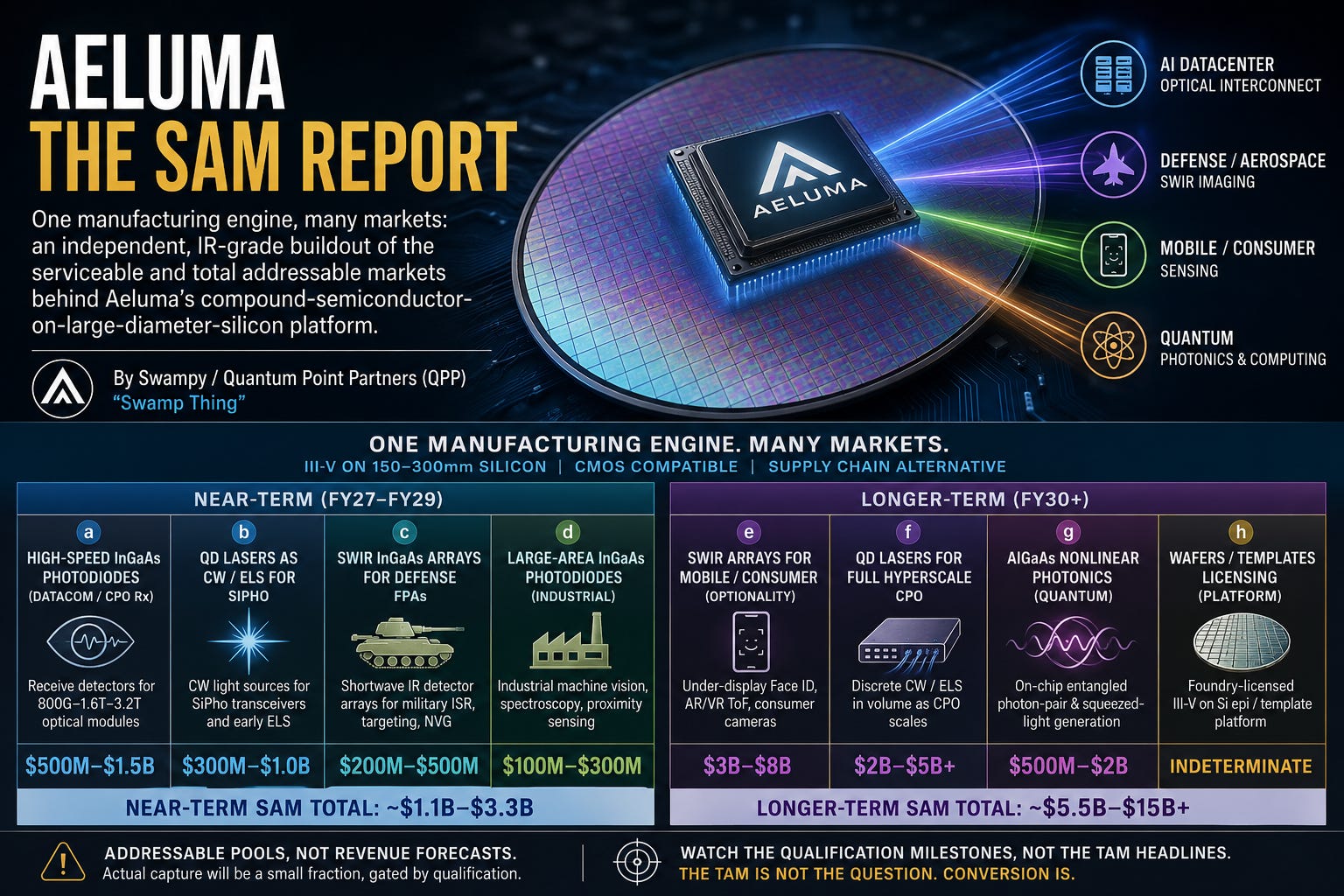

Aeluma. One manufacturing engine, many markets. The SAM Report

An independent, IR-grade buildout of the serviceable and total addressable markets behind Aeluma's compound-semiconductor-on-large-diameter-silicon platform

By Swampy / Quantum Point Partners (QPP) — "Swamp Thing"

Author's framing & a note on methodology

A few weeks ago, in the comments under one of my earlier Aeluma Notes, a reader and fellow ALMU enthusiast and investor, Greg, asked a deceptively simple question: could I break out a SAM range for each of Aeluma's product areas, and separate the near-term from the longer-term? I gave a rough first cut in the thread. This piece is the full, more complete version of that answer — the one Greg (and, I suspect, a few others) actually deserved.

This is the fourth piece in my running coverage of Aeluma. My prior Aeluma pieces laid out the platform thesis, walked through the foundry/partnership news flow, and reacted to the quantum/CHIPS developments. This one builds on all three and tries to put defensible numbers around the opportunity set.

Methodology and disclaimers (please read). Every SAM and TAM figure attributed to "the author," "my estimate," or "QPP" below is my own independent estimate. None of it is Aeluma guidance, Aeluma disclosure, or material non-public information. Where I cite third-party market sizes, I name the source and link it. I deliberately use published market-research forecasts (which diverge widely and should be treated as forecasts, not realized revenue) as external "anchors," and then apply my own judgment about what share Aeluma could serviceably address given its technology, partnerships, and qualification timeline. I draw on Aeluma's public filings and press releases, its Q3 FY2026 earnings call (quarter ended March 31, 2026), and one client-only sell-side report — Goldman Sachs Global Investment Research, Optical Networking: The next mega trend in AI infrastructure (17 April 2026) — which I paraphrase only and never reproduce. This is not investment advice. I hold no price target and make no buy/sell recommendation. See the full disclosure block at the end.

The thesis in one paragraph

Aeluma's core idea is to grow high-performance compound-semiconductor (III-V) materials — InGaAs photodiodes and detectors, quantum-dot lasers, AlGaAs nonlinear photonics — on large-diameter (up to 300mm), CMOS-compatible silicon substrates rather than on small, supply-constrained, expensive indium-phosphide (InP) or native GaAs wafers. The bet is that a single manufacturing "engine" can be pointed at many end markets: AI-datacenter optical interconnect, defense/aerospace SWIR imaging, mobile/consumer sensing, and quantum. If even one or two of those markets convert from "engagement" to "qualified design-in," the operating leverage on a roughly $4.5M revenue base is significant. The risk, equally, is that III-V-on-Si qualification cycles are long, incumbents are entrenched, and the consumer-SWIR optionality may never arrive.

Where Aeluma actually is today (the public record)

Before sizing the future, anchor the present. From Aeluma's Q3 fiscal 2026 results (quarter ended March 31, 2026; released May 13, 2026) and related filings:

Revenue: $1,222K for the quarter, versus ~$1.3M a year ago and ~$1.3M in the prior quarter; nine-month revenue ~$3.9M. Revenue is predominantly U.S.-government R&D contracts.

Profitability: GAAP net loss $1.8M, or $(0.10)/share; non-GAAP net loss $701K; adjusted EBITDA loss $911K.

Balance sheet: $37,780K cash and equivalents at 3/31/2026; no long-term debt. A $50M at-the-market (ATM) equity program was established via a sales agreement disclosed March 20, 2026 (undrawn at quarter-end).

Guidance: Full-year FY2026 revenue narrowed to $4.2–4.6M (from $4.0–6.0M), citing delays in contract execution related to government shutdowns, pushing revenue into FY2027.

Backlog/visibility: remaining performance obligations of ~$8.9M; six new contracts totaling ~$5M secured in FY2026, including >$4M from U.S. government agencies.

IP: 36 issued and pending patents (as of the Q3 FY2026 filing).

Pipeline: on the Q3 call CEO Jonathan Klamkin said the company's customer pipeline had grown from a previously mentioned ~20 engagements to upwards of 30 — concentrated in AI datacom, mobile SWIR, defense, and quantum.

Controls caveat: management disclosed that disclosure controls remained not effective due to limited finance staffing, with remediation underway.

Recent catalysts in the public record: a NASA award for integrated quantum-dot lasers (April 21, 2026); >$4M / six new government contracts to scale the heterogeneous-integration platform, announced alongside manufacturing partnerships with Tower Semiconductor (foundry) and Sumitomo Chemical Advanced Technologies (wafer/epi scaling) (April 13, 2026); AIM Photonics full membership (announced January 2, 2025, leveraging 300mm MOCVD onto AIM's 300mm silicon-photonics wafers); the Thorlabs large-diameter wafer partnership demonstrating wafer-scale AlGaAs on 200mm CMOS silicon (May 2025); and the May 28, 2026 commentary on the U.S. Department of Commerce's proposed CHIPS Act quantum incentives.

On the CHIPS quantum news, Aeluma stated it "supported one of the companies that executed a letter of intent with the U.S. Government," with any direct involvement contingent on the execution of a subcontract. Per NIST's May 21, 2026 release, the Department of Commerce announced the signing of 9 letters of intent to provide $2.013 billion in federal incentives under the CHIPS and Science Act — $1B to IBM (to establish a quantum foundry subsidiary, Anderon), $375M to GlobalFoundries (with the government also taking an equity position), and $100M each to Atom Computing, D-Wave, Infleqtion, PsiQuantum, Quantinuum and Rigetti, plus $38M to Diraq. I am deliberately not naming or speculating which of the nine LOI recipients Aeluma supports. Aeluma has chosen not to disclose the customer; I'll size the quantum line off platform capability and the program scale, not off any named end-customer.

The market backdrop: why now

The single most important macro fact for Aeluma's near-term lines is the AI-driven optical-interconnect boom and the supply tightness underneath it. On the Q3 call, Klamkin's framing was blunt: the AI data-center buildout is outpacing the photonics supply chain, major laser suppliers are sold out, and InP substrate supply is constrained — exactly the conditions that make a non-InP, large-diameter alternative interesting.

The sell-side now treats optical networking as a structural AI theme. Goldman Sachs Global Investment Research (Optical Networking, Apr 2026) frames an aggregate scale-up + scale-out networking value TAM rising roughly 9x — from about US$15bn (GB300 NVL72 generation, mainly 2026) to about US$154bn (Rubin Ultra NVL576, mainly 2028) — with co-packaged optics (CPO) contributing about US$91bn (~59%) of that $154bn, and CPO TAM totaling roughly US$97bn over 2026–28E on the high end. Goldman also tracks silicon-photonics penetration of datacom optical modules rising from about 6% in 1Q24 to roughly 45% by 4Q28E, and a speed migration from 800G to 1.6T (2026) to 3.2T+ (2027–2028), with CPO-with-switch commercial kickoff in 2026 (Nvidia Quantum-X / Spectrum-X Photonics; Broadcom Bailly/Davisson).

Crucially for Aeluma's laser line, Goldman's bill-of-materials work on a CPO switch puts external laser sources (ELS) at roughly 9% of CPO-switch BoM value (with optical engines ~43%), and frames per-unit ELS economics (ELS ~$400/unit; ~18 ELS per Quantum-X Photonics switch; CW lasers ~$30 each at ~300mW) — implying per-rack ELS dollar content for Rubin Ultra NVL576 scale-up of roughly $65k. Goldman expects light-source (EML and CW) supply tightness to persist through 2027 and balance around 2H28, in part because of InP substrate constraints and China-related export-control/geopolitical tension. Independent corroboration of the same supply story comes from TrendForce, which describes Nvidia pre-allocating EML capacity and an accelerating shift toward CW + silicon-photonics among non-Nvidia buyers.

Two further independent third-party anchors round out the laser/ELS picture. Northland Capital Markets analyst Tim Savageaux has sized the external-laser-source (ELS) opportunity at $1B+ annually (in Northland's coverage of the POET–Sivers ELS collaboration). And LightCounting projects that silicon-photonics-based transceivers will exceed 50% of optical-transceiver sales in 2026, up from 33% in 2024 (and 10% in 2018). These matter because Aeluma's quantum-dot-laser-as-CW-source thesis is a direct play on exactly the ELS/CW segment that these sources independently flag as the bottleneck.

The framework: TAM → SAM → timing/qualification

For each product line I move through three layers:

TAM (third-party). The broad end-market dollar pool, taken from named market-research forecasts or sell-side work. These diverge a lot — I show ranges and name sources rather than pretend to precision.

SAM (author's estimate). The slice Aeluma could serviceably address — the right wavelength, the right device, the right form factor, reachable through its foundry/packaging partners within the stated horizon. This is my judgment, not company guidance.

Timing & qualification gating. When the SAM becomes reachable, and what has to be true (process transfer, reliability qual, design-in) for revenue to follow.

I split the eight lines into NEAR-TERM (FY27–FY29) and LONGER-TERM (FY30+) buckets, mirroring Greg's original question.

NEAR-TERM SAM (FY27–FY29)

(a) High-speed InGaAs photodiodes for datacom / CPO receivers

What it is. The receive-side detector in optical transceivers and CPO optical engines — InGaAs PIN/APD photodiodes and arrays operating at 100G/lane and 200G/lane, supporting 800G→1.6T→3.2T modules. Klamkin noted on the call that Aeluma's high-speed InGaAs photodiodes and arrays can support both "slow and wide" and "fast and narrow" transceiver formats.

Third-party TAM context. Per MarketsandMarkets, the optical-transceiver market was valued at ~US$13.6B in 2024 and is projected to grow from ~US$15.6B in 2025 to ~US$25.0B by 2029, at a 13.0% CAGR. Fortune Business Insights sizes it larger over a longer horizon (~$14.7B in 2025 → ~$46B by 2034). The AI-specific optical-transceiver segment is larger and faster: per LightCounting's early-2026 work, the AI transceiver market reached ~$16.5B in 2025 and is set to reach ~$26B in 2026, a ~60% growth rate in both years. Photodiodes are a modest but essential fraction of module BoM; Goldman's CPO BoM work implies receive-side optics is a meaningful slice within the ~43% "optical engine" share.

Author's SAM estimate (FY27–29): $500M–$1.5B. This is the dollar value of high-speed InGaAs detector content that Aeluma could theoretically serve as the datacom/CPO receive market scales — not what it will capture. Actual capture in the window is likely a small fraction of this, gated entirely by qualification.

Key assumptions / gating factors. Requires reliability qualification at a module maker or hyperscaler, plus process transfer to a volume foundry (Tower is explicitly positioned for AI datacom among other markets). The supply-tightness backdrop (Goldman, TrendForce) is the tailwind; incumbent InP photodiode suppliers (Coherent, Lumentum) with 200G photodiode products already shipping are the headwind.

(b) Quantum-dot lasers as CW sources for SiPho transceivers / ELS

What it is. Continuous-wave (CW) light sources — Aeluma's MOCVD-grown quantum-dot (QD) lasers — feeding silicon-photonics modulators, either as discrete CW lasers or, longer-term, as external laser sources (ELS) for CPO. Management claims to be first to offer MOCVD QD lasers (higher throughput than MBE), being evaluated for power handling, reliability, and packaging simplicity.

Third-party TAM context. Northland's Savageaux pegs the ELS market at $1B+ annually. Goldman's ELS economics (~9% of CPO-switch BoM; ELS ~$400/unit; ~18 per Quantum-X Photonics switch) put a credible per-system dollar figure on the segment. A typical 800G/1.6T SiPho module uses 2–4 CW sources at ~$8–10 each (per DeepFundamental's teardown), so volume, not unit price, drives this market.

Author's SAM estimate (FY27–29): $300M–$1.0B. The lower bound reflects the discrete-CW-laser opportunity at current SiPho attach rates; the upper bound captures early ELS ramp and aligns with the $1B+ ELS anchor. I am deliberately keeping the top of my range at, rather than above, the headline ELS number because QD-laser CW power handling for full CPO is still being validated — Aeluma's own materials describe high power handling and reliability as attributes still under evaluation, so I treat the near-term high-power CPO use case as unproven.

Key assumptions / gating factors. The AIM Photonics government-directed project (QD laser on 300mm SiPho) and the NASA QD-laser award de-risk the technology; conversion needs a transceiver/CPO customer qualification. Competition: InP DFB CW incumbents (Coherent's 6-inch InP fab ramp in Sherman, Texas) and alternative CW suppliers (Lumentum, and high-volume Chinese suppliers).

(c) SWIR InGaAs photodiode arrays for defense focal-plane arrays (FPAs)

What it is. Shortwave-infrared (0.9–1.7µm) InGaAs detector arrays for military ISR, targeting, and night-vision FPAs — Aeluma's dual-use sweet spot, where 150mm wafers are often sufficient and government R&D contracts already fund development.

Third-party TAM context. Per Grand View Research, the short-wave infrared cameras & sensors market was estimated at ~US$328.4M in 2024 and is projected to reach ~US$620.2M by 2030, at an 11.3% CAGR, with the defense & military segment holding the largest revenue share in 2024 and FPAs a fast-growing product segment. Scope-dependent alternatives diverge sharply: narrower SWIR-camera-only scopes come in below $150M, while broader InGaAs SWIR sensor categories reach $2B+ by mid-decade. The Grand View component/sensor scope is the closest match to Aeluma's component-level position, which is how I anchor my SAM below.

Author's SAM estimate (FY27–29): $200M–$500M.Component-level InGaAs FPA content addressable through defense primes and defense-tech customers, where Aeluma's cost/scale story and U.S.-domestic posture are differentiators.

Key assumptions / gating factors. This is the line with the clearest path because government contracts already fund it and qualification standards, while rigorous, are familiar to Aeluma. Klamkin described several programs progressing to "later stage" technology-transition phases. Gating: transition from development contract to production purchase order; competition from incumbent InGaAs FPA makers (Teledyne, Lynred, Sensors Unlimited).

(d) Large-area InGaAs photodiodes for industrial / proximity sensing

What it is. Larger-area InGaAs detectors for industrial machine vision, spectroscopy, and proximity/range sensing — a steadier, less glamorous commercial market.

Third-party TAM context. Carved from the same InGaAs sensor pool above; the industrial slice is the second-largest application after defense in most reports. For reference, the InGaAs camera market is sized at roughly $180M in 2024 → ~$372M by 2032.

Author's SAM estimate (FY27–29): $100M–$300M. A modest but real near-term commercial beachhead.

Key assumptions / gating factors. Lower qualification barrier than datacom or mobile; price competition is the main risk. Useful as early commercial revenue while bigger lines qualify.

LONGER-TERM SAM (FY30+)

(e) SWIR imaging arrays for mobile / consumer (under-display Face ID, AR/VR ToF)

What it is. The big optionality line: InGaAs SWIR arrays integrated at scale for mobile (under-display 3D sensing/Face ID), AR/VR time-of-flight, and consumer cameras — leveraging Aeluma's large-diameter, CMOS-compatible, cost-down manufacturing. This is the use case where "III-V on 300mm Si" matters most, because consumer economics demand wafer scale.

Third-party TAM context. There is no clean third-party number for "consumer SWIR" because the market does not meaningfully exist yet. I anchor instead off the scale of mobile-sensing semiconductors broadly and the fact that VCSEL-based 3D sensing (today's Face ID) is already a multi-billion-dollar category. Aeluma itself frames MOCVD as the same tool proven for VCSELs used in phone facial-ID. On the call, Klamkin said Tower's foundry could support mobile/consumer among other markets.

Author's SAM estimate (FY30+): $3B–$8B if mobile OEMs broadly adopt SWIR. I want to be explicit: this is optionality, not a base case. The range is large because the outcome is binary — either a major OEM designs SWIR into a flagship platform (huge) or it doesn't (near-zero). Treat the entire line as a call option.

Key assumptions / gating factors. Requires a flagship OEM design-win, multi-year qualification, and cost parity — none of which are visible today. This is the highest-variance line in the model.

(f) Quantum-dot lasers for full CPO deployment at hyperscale

What it is. The scaled-up version of line (b): QD lasers (discrete CW or integrated ELS) shipping in volume as CPO moves from pilots to hyperscale deployment across 2027–2030.

Third-party TAM context. Goldman's CPO TAM (~US$97bn cumulative 2026–28E high-end; ~US$91bn CPO within the $154bn 2028 networking TAM) is the headline anchor; ELS at ~9% of CPO-switch BoM implies a multi-billion-dollar ELS pool as CPO scales. Independent CPO market forecasts vary enormously — IDTechEx (>US$20B by 2036, 37% CAGR), Mordor Intelligence (~$161M in 2026 → ~$749M by 2031), Precedence (~$95M in 2025 → ~$1,055M by 2034), and others ranging into the multiple billions by 2030 — which underscores how uncertain both the size and the timing are. Present these as a range, not a consensus.

Author's SAM estimate (FY30+): $2B–$5B+ as CPO ramps.Again, this is the addressable pool, not capture.

Key assumptions / gating factors. Depends on (1) CPO actually ramping on schedule — far from certain given packaging/yield barriers — and (2) QD lasers closing the CW power-handling gap for CPO, which remains unproven at the power levels full hyperscale CPO demands. Competition from vertically integrated CPO players (Nvidia/TSMC COUPE, Broadcom) and InP ELS incumbents is intense.

(g) AlGaAs nonlinear photonics for quantum computing

What it is. AlGaAs nonlinear photonic circuits — for on-chip entangled-photon-pair and squeezed-light generation via χ⁽²⁾/χ⁽³⁾ nonlinearities — integrated wafer-scale on CMOS silicon (the Aeluma/Thorlabs 200mm compound-semiconductor-on-insulator demonstration). AlGaAs offers materially stronger optical nonlinearity than silicon nitride or thin-film lithium niobate; peer-reviewed work (UCSB, PRX Quantum, 2021) demonstrated AlGaAs-on-insulator photon-pair sources with internal generation rates exceeding 20×10⁹ pairs/sec/mW² and >99% purity, far above the best silicon-nitride sources.

Third-party TAM context. Per Mordor Intelligence, the quantum-photonics market stood at ~US$0.85B in 2025 and is forecast to reach ~US$3.78B by 2030, advancing at a 34.5% CAGR, with the quantum-computing application its largest pillar (~$1.5B by 2030) and communication ~$1.3B by 2030. Global Market Insights sizes photonic quantum computing at ~$175.7M in 2025 → ~$1.5B by 2031 (40% CAGR). A separate Research & Markets report projects photonic QC revenues of ~$1.1B by 2030 rising to >$7B by 2036. There is no published standalone dollar TAM for AlGaAs nonlinear photonics — it sits inside the nonlinear/III-V and PIC sub-segments — so any number here is inferential. The relevant policy anchor is the U.S. DoC's $2.013B CHIPS quantum LOI program (May 2026; nine companies, including IBM $1B and GlobalFoundries $375M for quantum foundries). Note that among the field, both squeezed-light/continuous-variable players and entangled-photon/discrete-variable players rely on exactly the χ⁽²⁾/χ⁽³⁾ nonlinear sources AlGaAs targets — but public sources do not state which company Aeluma supports, and I am not inferring it.

Author's SAM estimate (FY30+): ~$500M–$2B by 2030.This is a platform-capability estimate keyed off the quantum-photonics component pool and the public-funding wave, not off any named end-customer.

Key assumptions / gating factors. Earliest revenue likely flows through government/foundry programs (the CHIPS subcontract path Aeluma flagged, contingent and milestone-based) rather than commercial product sales. Squeezed-light/photon-pair architectures are still pre-commercial; this line is real but long-dated.

(h) Large wafers and templates as a foundry-licensed platform

What it is. The "arms-dealer" model: licensing Aeluma's large-diameter III-V-on-Si epi/template platform to foundries and integrators rather than (or alongside) selling finished devices. Sumitomo (wafer/epi scaling) and Tower (foundry) are the visible building blocks.

Third-party TAM context. Not sizable in the conventional sense — value depends entirely on licensing/royalty structure, which is undisclosed.

Author's SAM estimate: indeterminate — depends entirely on licensing terms. I am not putting a number on this; it is a structural optionality that could be high-margin if it materializes but is unmodelable today.

Key assumptions / gating factors. Requires a defined licensing model and a partner willing to pay for the platform. Upside: capital-light, recurring. Risk: cannibalizes device economics; IP enforcement.

Aggregate SAM summary (author's independent estimates)

The table below sums my serviceable-market ranges. Critical caveat: these are addressable pools, not revenue forecasts.Aeluma's actual near-term capture will be a small fraction, and the lines are not additive in a simple way (the QD-laser near-term and long-term lines overlap conceptually). I show them grouped as Greg asked.

#Product lineHorizonAuthor SAM rangePrimary 3rd-party anchoraHigh-speed InGaAs PDs (datacom/CPO Rx)FY27–29$500M–$1.5BOptical transceiver TAM (MarketsandMarkets $15.6B→$25.0B); Goldman CPO BoMbQD lasers as CW/ELS for SiPhoFY27–29$300M–$1.0BELS $1B+ (Northland/Savageaux); Goldman ELS BoMcSWIR InGaAs arrays for defense FPAsFY27–29$200M–$500MSWIR sensors (Grand View $328M→$620M)dLarge-area InGaAs PDs (industrial)FY27–29$100M–$300MInGaAs camera market (~$180M→$372M)Near-term subtotalFY27–29~$1.1B–$3.3BeSWIR arrays for mobile/consumerFY30+$3B–$8B (optionality)Mobile 3D-sensing analoguefQD lasers for full hyperscale CPOFY30+$2B–$5B+Goldman CPO TAM (~$91–97bn)gAlGaAs nonlinear photonics (quantum)FY30+$500M–$2BQuantum photonics (Mordor $0.85B→$3.78B by 2030)hWafers/templates licensingn/aIndeterminateLicensing-structure dependentLonger-term subtotalFY30+~$5.5B–$15B+

Read this as a map of where the platform could play, sized against named external anchors — not as a revenue bridge.

From SAM to revenue: the gating milestones

A SAM is worthless without a path to capture. Here is what I'll be watching, roughly in order of how much each would de-risk the story:

Foundry process transfer & yield. The Tower (foundry) and Sumitomo (wafer/epi) relationships have to convert from announcements into qualified, yielding process flows at 150/200/300mm. This is the single biggest unlock.

First qualified design-in. Management was candid that no customer qualification is yet complete. The first formal qual — most plausibly in defense FPAs or a discrete CW laser — would be the inflection from R&D revenue to product revenue.

Reliability qualification. Datacom and especially CPO demand brutal reliability/lifetime data. QD-laser power-handling and reliability validation is the gating item for lines (b) and (f).

CHIPS/quantum LOI → funded subcontract. Aeluma's stated involvement is contingent on a subcontract. Conversion of that relationship into funded work would validate line (g) without Aeluma needing to name the customer.

Licensing structure. Any disclosed licensing/royalty model would put a number on line (h) for the first time.

Benchmarks that would move my view: a first named production PO (bullish); a completed customer qualification (very bullish); slippage in CPO timelines or a competitor locking in QD/ELS sockets (bearish); ATM drawdown materially above what's needed to fund qualification (dilution watch).

Risk register (candid)

Tiny revenue base. $4.2–4.6M FY2026 guided revenue against multi-billion-dollar SAMs. The gap between addressable and captured is the whole story, and it is enormous.

Dilution. The $50M ATM is undrawn but available; ongoing losses (~$0.9M quarterly adjusted EBITDA loss) mean equity issuance is a live risk even with $37.8M cash.

Multi-year qualification cycles. No customer qual is complete; III-V-on-Si reliability validation is measured in years, not quarters.

Consumer-SWIR is optionality, not base case. Line (e), the largest single SAM, is a binary OEM bet that may never convert.

Incumbent competition. Coherent, Lumentum (InP lasers/photodiodes), Teledyne/Lynred (SWIR FPAs), and vertically integrated CPO players (Nvidia/TSMC, Broadcom) are formidable and already shipping.

Wide third-party TAM uncertainty. The market-research forecasts I cite diverge by 5–10x in places (especially CPO and SWIR), so the anchors themselves are soft.

Customer concentration. Revenue is concentrated in U.S.-government customers; contract timing (e.g., shutdown-driven delays) directly hit guidance this year.

Controls. Management disclosed disclosure controls were not effective due to limited finance staffing — a governance item to watch as the company scales.

Geopolitics cuts both ways. InP/China supply tension helps the "alternative substrate" thesis but also injects macro volatility into the whole optical supply chain.

Closing

Aeluma is, today, a sub-$5M-revenue R&D-funded company with an unusually broad and credible platform thesis sitting in front of several genuinely enormous markets at exactly the moment those markets are supply-constrained. The bull case is the operating leverage if one or two lines qualify; the bear case is that qualification never quite arrives, or arrives too slowly, while the ATM funds the wait. My SAM ranges above are meant to frame the size of the prize per line — explicitly as my own estimates, anchored to named third-party data and the Goldman optical-networking framework — not to predict capture. For Greg, and for anyone else doing the work: watch the qualification milestones, not the TAM headlines. The TAM is not the question. Conversion is.

References & links

Aeluma — primary sources

Q3 FY2026 earnings press release (8-K Exhibit 99.1, May 13, 2026): sec.gov

Form 8-K (results, May 13, 2026): sec.gov

Form 10-Q (period ended March 31, 2026): sec.gov

Q3 FY2026 earnings call / transcript hub: marketbeat.com

NASA award for integrated quantum-dot lasers (Apr 21, 2026): aeluma.com

$4M contracts + Tower Semiconductor & Sumitomo Chemical partnerships (Apr 13, 2026): aeluma.com

AIM Photonics full membership (Jan 2, 2025): aeluma.com

Thorlabs AlGaAs-on-200mm CSOI breakthrough (May 29, 2025): aeluma.com

CHIPS quantum commentary (May 28, 2026): manilatimes.net

Thorlabs/AlGaAs technical detail (SPIE Photonics West): spie.org

Policy / government

NIST/DoC — 9 CHIPS quantum LOIs, $2.013B (May 21, 2026): nist.gov

IBM — first purpose-built quantum foundry (Anderon), proposed $1B CHIPS award: newsroom.ibm.com

Third-party market anchors

Optical transceiver TAM — MarketsandMarkets ($13.6B 2024 → $15.6B 2025 → $25.0B 2029, 13.0% CAGR): marketsandmarkets.com

Optical transceiver (longer horizon) — Fortune Business Insights (~$14.7B 2025 → ~$46B 2034): fortunebusinessinsights.com

AI transceiver growth & SiPho >50% share by 2026 — LightCounting: May 2026; Nov 2025

ELS ~$1B+ annual opportunity — Northland Capital Markets (Tim Savageaux), via POET–Sivers ELS collaboration release: poet-technologies.com

SWIR cameras & sensors TAM — Grand View Research ($328.4M 2024 → $620.2M 2030, 11.3% CAGR): grandviewresearch.com

Quantum photonics TAM — Mordor Intelligence ($0.85B 2025 → $3.78B 2030, 34.5% CAGR): mordorintelligence.com

Goldman Sachs Global Investment Research, Optical Networking: The next mega trend in AI infrastructure (17 April 2026); figures are paraphrased and no tables or substantial text are reproduced. You can find the report here:

GOLDMAN SACHS RESEARCH Optical Networking: The Next Mega Trend in AI Infrastructure

Disclosure & disclaimer

This article is independent research published by Swampy / Quantum Point Partners (QPP), brand "Swamp Thing," at quantumpointpartners.substack.com. It is for informational and educational purposes only and is not investment advice, nor an offer or solicitation to buy or sell any security. All SAM/TAM estimates designated as the author's are independent estimates, are not Aeluma guidance, disclosure, or representation, and may be wrong. Third-party market-size figures are attributed to their sources and are forecasts that diverge widely. References to Goldman Sachs Global Investment Research (Optical Networking, Apr 2026) are paraphrased; no tables or substantial text are reproduced. This piece contains no material non-public information; where Aeluma has chosen not to disclose a counterparty (e.g., the CHIPS quantum LOI recipient), the author has not speculated as to its identity. The author holds no price target and makes no buy/sell recommendation. The author may hold positions in securities mentioned; readers should assume the author is not objective and should do their own research and consult a licensed financial advisor. Figures should be independently verified against primary sources before any decision.

Nice article. One thing I found particularly interesting in this analysis is that it implicitly shifts the discussion away from photonic performance and toward qualification and manufacturing scalability.

Most investors still seem focused on whether III-V devices can outperform existing solutions. Increasingly, I find myself asking a different question: if AI optical infrastructure continues scaling as projected, where does the next manufacturing bottleneck emerge?

If the industry ultimately becomes constrained by foundry portability, wafer-scale integration, qualification throughput, packaging complexity, or optical manufacturing capacity rather than device physics itself, the value may accrue very differently than most current models assume.

Curious which of the eight opportunity areas you believe is most likely to achieve qualification first. Defense SWIR appears to have the shortest path, while datacom and CPO arguably offer the largest long-term upside. Which market do you believe is most likely to validate the platform initially?